Impact of RWA's in DeFi: Part 1

- Why is on-chain RWA one of the most important milestones in DeFi?

- How will RWA reshape the DeFi landscape?

- What will RWA adoption change for us: DeFi users and builders?

- Which protocols should we follow for the RWA narrative?

—————————————————————————————

As DeFi grows, developers are adding more and more new building blocks that are necessary for creating a new, accessible and beneficial financial system. In recent months, particular attention has been paid to RWAs as a potentially game-changing direction for DeFi.

Outlook on the current state of DeFi and RWA in TradFi

To see why this could truly transform the state of affairs and help take the next big step in the development of the global financial system, it is necessary to understand what the RWA sector entails and assess it in the context of DeFi. What you should know:

— Real World Assets include a vast array of assets such as commodities, real estate, treasury bills, private credit, artwork, equipment and intellectual property. [1]

— The size of the private credit market in 2023 is approximately $1.4 trillion with $350 billion of the capital under management is waiting to be deployed. It is expected to grow to $2.3 trillion by 2027. [2] [3]

— The real estate market in US alone is projected to reach a value of $113.60 trillion in 2023. The residential real estate market is estimated at $88 trillion.[4] [5]

— The gross amount of new T-bills issued in December 2020 was $1,591 billion, while the average daily trading volume for T-bills on secondary market has exceeded $75 billion since 2001.

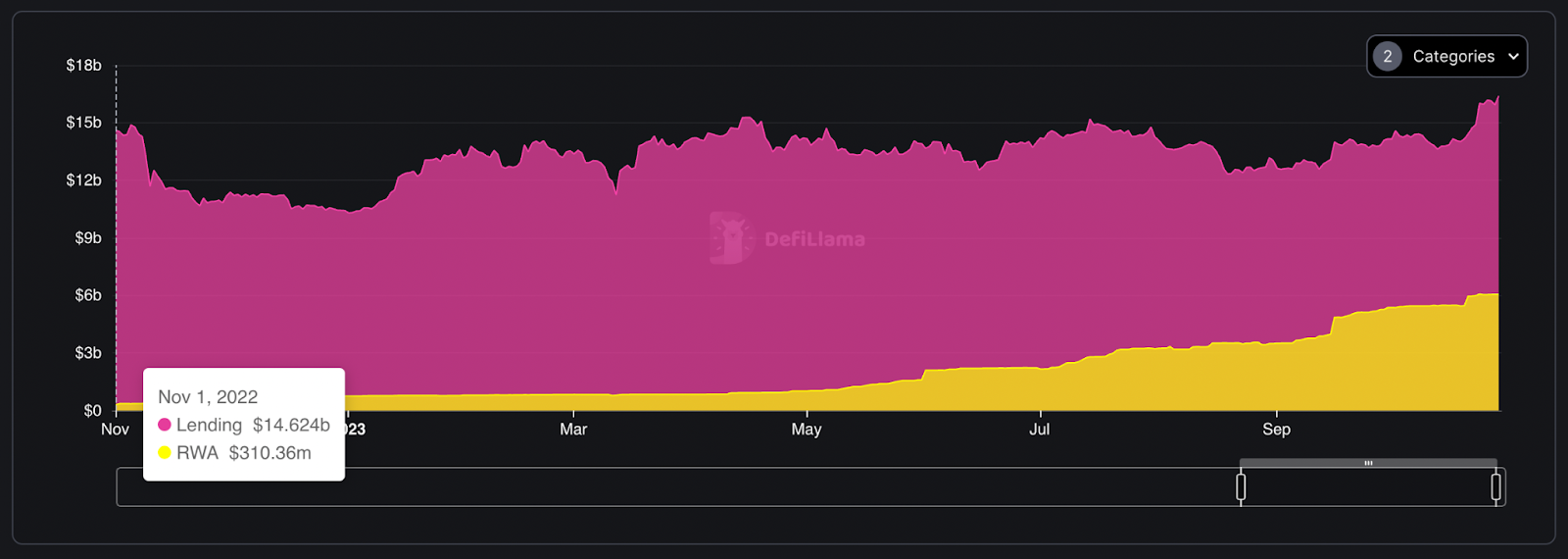

— Current Total Value Locked (TVL) in DEXs is $12.333b, in Lending protocols it is $18.43b, and RWA combines $5.935b in locked value [6]

Source: DefiLlama

— The only formed and established DeFi categories are DEX, Lending and Liquid Staking (LSD), exceeding >$10b in value

— The value locked in RWA in DeFi has nearly doubled in 2023, with the majority coming from yield-bearing assets like Treasuries, real estate, and private credit [7]

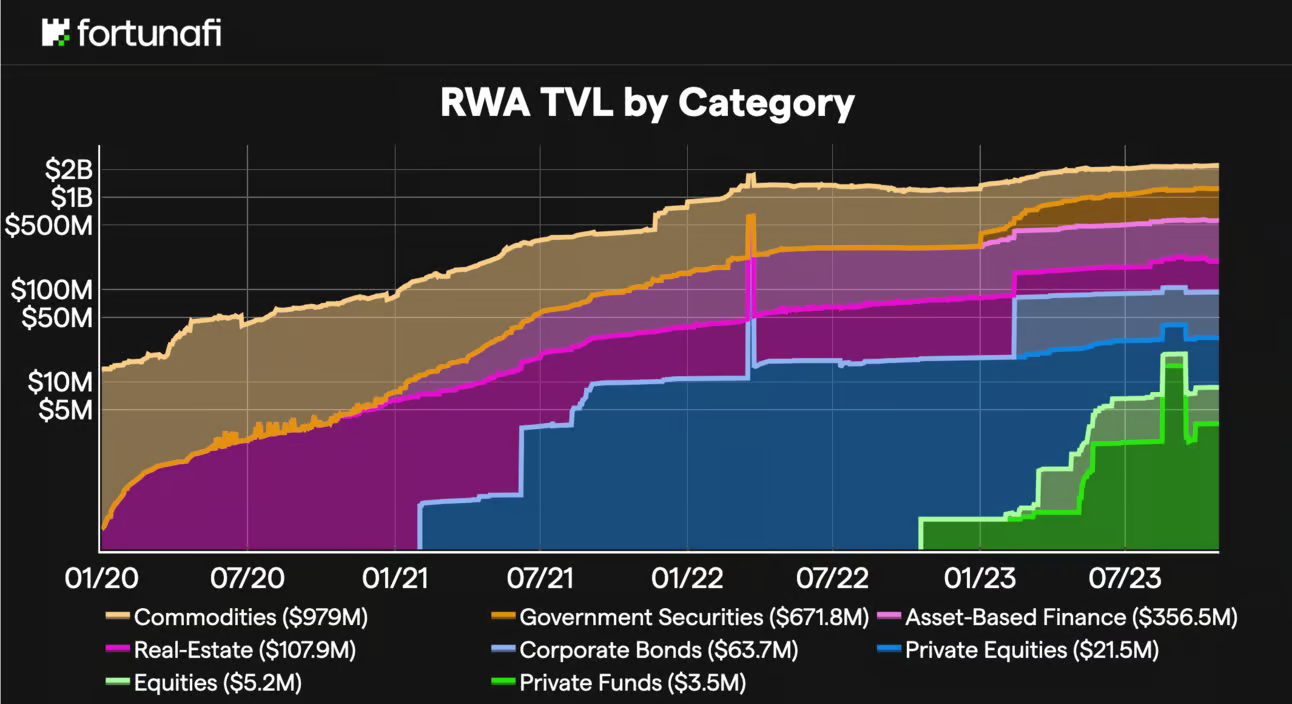

Source: Fortunafi

These demonstrate the huge scale of RWA in the TradFi sector, indicating the potential that lies in tokenizing these assets for the DeFi. The existing and projected growth within each sector underscores the importance of RWAs and the significant role they play in the global financial ecosystem. The market for tokenized assets could reach $3.5 trillion in a conservative estimate and up to $10 trillion by 2030.

How Real World Assets fit the on-chain economy?

Let’s look at 3 TradFi products — Treasury Bills, Private Credit Investments and Real Estate — to understand RWA potential, use cases and why it makes sense to bring real world assets on-chain.

Treasury Bills (T-Bill)

T-Bills provide TradFi with short-term and risk-free investment tool, that also can be used for liquidity management. In addition, T-Bills serve as a benchmark for determining short-term interest rates and are used to guide the pricing of other financial products.

Treasury bills can be tokenized, converting the rights to the cash flows from the government securities into digital tokens

Problems solved on chain:

- Slow settlements in TradFi: DeFi's near-instant settlement of on-chain T-bill eliminates the days-long wait of traditional systems, reducing counterparty risk and increasing capital efficiency.

- High entry barriers for T-bills: DeFi opens T-bill investment to a wider audience through tokenization, allowing for fractional ownership and investment with minimal capital, thus democratizing access.

- Prohibitive costs of T-bill transactions: DeFi cuts down on the transaction fees and administrative costs associated with T-bills by removing intermediaries, making transactions more cost-effective for investors.

Use cases for tokenized T-Bills:

Full assurance and automation: Smart contracts can be used to automatically issue funds once the T-bills have matured, providing full transparency and assurance that the T-bills can be claimed.

Issuance of stablecoins: T-bills can serve as collateral for stablecoins and other crypto assets. For example, a smart contract could issue USDT with T-bills as collateral, maintaining a 1:1 peg to the USD.

Collateralization: T-bills will be used as collateral in lending and borrowing protocols, allowing users to borrow against them for use in yield farming, ultimately enhancing capital efficiency.

Trading on secondary markets: This enables easier access to T-bills, especially for those outside of the US, and creates more incentives to purchase T-bills since they can be readily sold if desired.

Automated yield management strategies: In TradFi, the provider of the T-bill manages the trading strategy of the treasury bond reserve. Investors unable to manually manage their trading strategy will purchase tokenized T-bills and be assured that the yield they receive has been automatically optimized.

Protocols to look at:

Perimeter Protocol. Blurb. Opentrade utilises Perimeter Protocol (Made by Circle who made USDC), For every tokenised t-bill that is purchased, the company will buy an actual t-bill and provide an onchain identifier for the underlying asset. The protocol also allows secured lending of USDC against their t-bills .

Fortunafi — A protocol delivers all-in-one liquidity solutions for stablecoin issuers, protocol treasuries, and traditional entities and offer a variety of investment products, such as private and public debt funds with native minting and redemption on the top blockchains.

Flux Finance — A protocol enables lending and borrowing of stablecoins against tokenized US Treasuries.

Maple Finance — An institutional capital network that provides the infrastructure for credit experts to run on-chain lending businesses and connects institutional lenders and borrowers.

Private Credit Investments

Private credit enables higher yield and customisable terms though direct loans, bypassing bank lending and can be used for diversification purposes on one side and for growth, acquisitions, refinancing and other corporate purposes on other side.

Problems solved on chain:

- Limited accessibility to Private Credit: DeFi enables wider participation in private credit markets by tokenizing debt, facilitating fractional ownership, and allowing for smaller investment thresholds.

- Inefficiencies in Private Credit allocation: Through the use of smart contracts, DeFi streamlines the process of matching borrowers with lenders, enhancing the efficiency of capital allocation and reducing operational overhead.

- Opacity in Private Credit markets: DeFi introduces transparency into private credit investments by recording transactions on a blockchain, providing clear audit trails, and improving risk assessment.

Use cases for Private Credit on-chain:

Unsecured Private Credit: This option enables borrowing liquidity without the need for full/over collateralization, leading to higher capital efficiency. Unsecured private credit protocols achieve this through centralized vetting of borrowers, including credit assessments and financial statement analysis. It's particularly beneficial for those who don’t have direct access to all their capital in liquid.

Asset-Backed Private Credit: This approach allows the use of RWA as collateral instead of solely relying on crypto assets. It's especially advantageous for borrowers who are underserved by traditional financial markets or those without access to a stable value store in their native currency.

Protocols to look at:

Centrifuge — An infrastructure that facilitates the decentralized financing of real-world assets natively on-chain, creating a fully transparent market which allows borrowers and lenders to transact without unnecessary intermediaries.

Goldfinch — A decentralized credit protocol that allows for crypto borrowing without crypto collateral—with loans instead fully collateralized off-chain.

Clearpool — A protocol’s permissionless single-borrower pools enable institutions to raise short-term capital while providing DeFi lenders access to risk-adjusted returns based on interest rates derived by market consensus.

Real Estate

Real Estate can be used for asset-backed lending and Investment Trusts (REITs) while also offers exposure to the market through Mortgage-Backed Securities (MBS) without requiring direct property ownership. The most logical method of tokenizing real estate is through the use of NFTs or fungible tokens. The process looks like this:

- 1. Obtain an official valuation from a trusted off-chain source.

- 2. Bridge this data to the blockchain via oracles.

- 3. Tokenize the asset into ERC-721 or ERC-20, based on the use case.

Problems solved on chain:

- Illiquidity of Real Estate assets: DeFi addresses the traditionally high illiquidity of real estate and allows for the fractionalization and smoother trading of property interests.

- High transaction costs and complexities: DeFi simplifies real estate transactions by cutting out numerous intermediaries, thereby reducing associated fees and streamlining the buying and selling process.

- Limited access to global markets: DeFi provides a global platform for real estate investment, breaking down geographical barriers and offering exposure to international property markets through a unified blockchain-based system.

Use cases for on-chain Real Estate:

A Single Real Estate Property as an NFT: Ownership of the NFT equates to ownership of the property, complete with a history of ownership, purchase records, and other suitable updates. This significantly streamlines the process of buying and selling properties, bypassing many of the complex legal procedures inherent in traditional real estate transactions.

Fractionalized Real Estate: High costs and the requirement to purchase entire properties often make real estate investment inaccessible. Fractional ownership circumvents this barrier, allowing individuals to hold tokens that represent a specific share of a property, making investment more attainable.

Tokenized Real Estate Cash Flow: The cash flow rights of a property can be tokenized as an NFT, which automates the distribution of funds to the holder transparently, ensuring a direct and clear transfer of rental income or profits.

Protocol to look at:

Tangible — The protocol offers users access to tokenized and fractionalized RWAs through their marketplace, utilizing Real USD, a native yield stablecoin backed by real estate.

Lofty — A marketplace that lets anyone invest in U.S. rental properties for only $50.

RealT — A platform to buy into the US real estate market through fully-compliant, fractional, tokenized ownership.

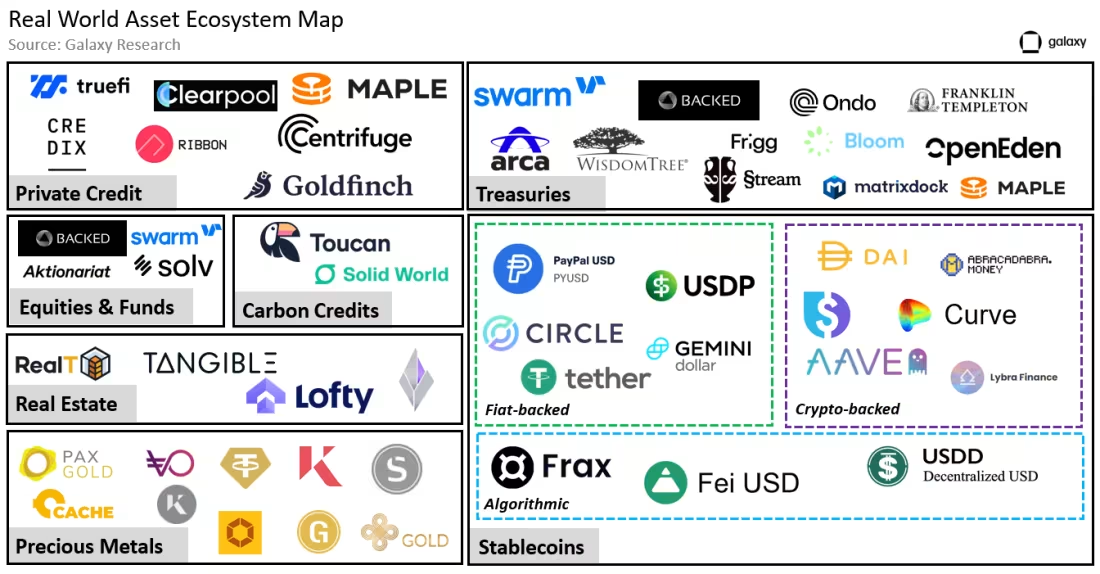

Source: Galaxy.com

A look into the future

Or Synergy of RWA and DeFi

What to expect when DeFi adapts RWA

The integration of Real World Assets into decentralized finance heralds a transformative era for financial markets. Below, we explore the multifaceted benefits that RWA adoption brings to Traditional Finance, the DeFi ecosystem, and stakeholders including investors, users, and builders.

For Traditional Finance:

Enhanced asset liquidity: Tokenization of illiquid assets like real estate or art facilitates easier trading, providing a liquidity boost to assets traditionally locked up for long periods.

Operational efficiency: Blockchains streamline transactions, cutting down on processing time and reducing the need for intermediaries.

Global reach: Tokenized RWAs can be accessed globally, transcending geographical barriers and opening up international markets for TradFi assets.

For the DeFi ecosystem:

Influx of fresh liquidity: RWA integration introduces new capital into DeFi, fueling the development and operation of dApps.

User base expansion: Familiar asset classes attract 'normies' to DeFi, enhancing adoption and broadening understanding of DeFi investments.

New collateral class: RWAs present new collateral types for DEXs, lending and borrowing, bolstering the robustness of DApps.

Rise of new products an concepts: The tokenization of RWAs paves the way for novel DeFi business and building opportunities, spurring economic growth.

Smoother onboarding for Institutions: On-chain RWAs mitigate institutions' entry barriers into DeFi by offering risk management tools and investment options they're already familiar with, thus reducing friction and fostering institutional participation.

For users and builders:

Innovative DeFi Products: RWAs unlock the potential for new DeFi offerings, diversifying investment portfolios.

New Yield Strategies: RWA enables unique yield farming strategies, including stable, real yield.

Sustainable Liquidity: RWA provide opportunities for liquidity retention through methods like refinancing of yield assets, ensuring a steadier flow of capital.

Regulatory Alignment: The integration of RWA will encourage regulatory frameworks that recognize DeFi, fostering legal clarity and investor confidence.

Risk Mitigation: The tangible nature of RWAs introduces a stabilizing factor to the volatile DeFi market, offering a hedge against market downturns.

What’s the Entangle contribution to the RWA adoption?

Entangle plays a crucial role in the adoption of Real-World Assets (RWAs) in the decentralized finance (DeFi) ecosystem, serving as a key facilitator of data communication between traditional finance (TradFi) businesses and decentralized applications (DApps). This integration is pivotal for implementing a variety of use cases, as it ensures a seamless and accurate flow of data across off- and on-chain environments.

Contribution to Treasury Bills

In the Treasury Bills sector, Entangle introduces industry changing advancements. It provides real-time price feeds, offering immediate updates on T-Bill values. This feature is particularly vital because T-Bill values fluctuate with changes in interest rates and market demands. Accurate and up-to-the-minute data allows investors to make informed decisions, and ensures that DeFi protocols represent the value of T-Bills correctly with corresponding tokens.

Furthermore, Entangle leverages the power of smart contracts to automate the entire lifecycle of T-Bills within the DeFi space. This automation spans from issuing digital tokens that represent the T-Bills to managing trades and ensuring that payments are made when the T-Bills mature. Such automation drastically reduces the need for manual processing, a common source of errors in the traditional financial system.

Contribution to Private Credit Investments

For Private Credit, Entangle offers transformative benefits. It enhances the efficiency of matching borrowers with lenders, a process that is often inefficient and opaque in traditional finance. By securely integrating off-chain data, such as credit scores and financial histories, into the on-chain environment, Entangle facilitates better decision-making in the lending process, not only widening the access to private credit but also allows lenders to assess risks more effectively.

Additionally, Entangle brings about transparency and efficiency in the market by recording all transactions on the blockchain. This level of transparency allows investors to monitor the performance of their loans and assess risks in real-time, marking a significant improvement over the often opaque private credit markets in traditional finance.

Contribution to Real Estate

In the Real Estate sector, Entangle's role is equally pivotal. It brings accurate real estate valuations onto the blockchain through oracles that pull data from trusted off-chain sources. This ensures that tokenized real estate is priced fairly, reflecting its true market value.

Moreover, Entangle simplifies the trading of real estate by enabling the tokenization of property interests. This innovation has the potential to revolutionize the real estate market by removing numerous barriers to entry for investors and speeding up real estate transactions, making them as straightforward as trading stocks.